")

")

")

")

Nikada

Ladder Capital (NYSE:LADR) is a leading mortgage REIT that provides capital for the commercial real estate sector. The REIT chiefly invests in senior secured loans, which are secured by commercial real estate and which provide Ladder Capital with regular interest income. Ladder Capital as well as the broader commercial real estate industry may see easing headwinds in 2024 as the Federal Reserve is set to reduce interest rates, but I don’t expect the REIT to increase its dividend next year. Since shares are now trading close to book value, 0.96X P/B, I believe the risk profile is not attractive enough to maintain a buy recommendation at this point!

Previous coverage

I worked on Ladder Capital two and a half years ago, in 2021, and recommended shares to investors focused on generating income: 7.0% Yield And Potential For A Revaluation. Ladder Capital had a chance, I argued at the time, to reduce the gap that existed at the time between share price and accounting book value. Since shares of Ladder Capital trade at 0.96x BV now, as opposed to 0.8X BV in May 2021, I am downgrading my rating to hold.

Ladder Capital is a leading CRE capital provider with a commercial loan-focus

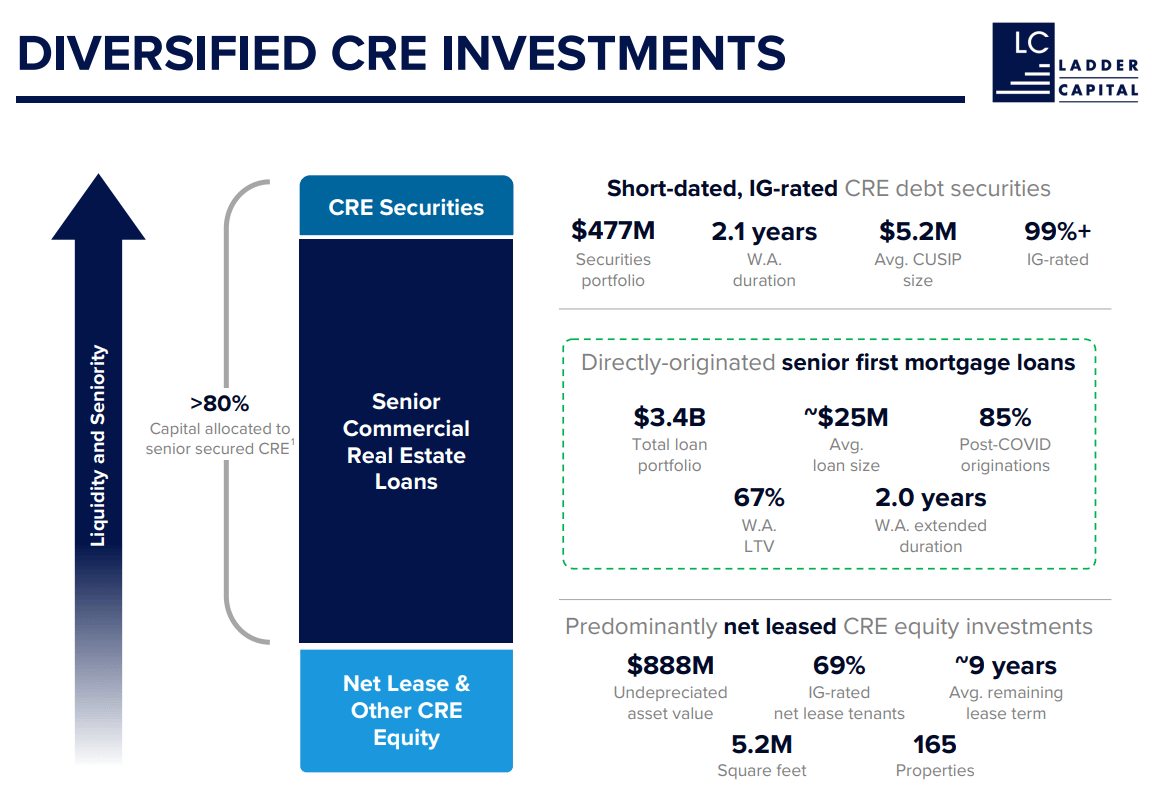

Ladder Capital provides liquidity and capital to the commercial mortgage market and owns approximately $5.5B in assets. The main foundation of the REIT’s portfolio is senior secured loans that were valued at $3.4B at the end of the September quarter. Besides loans to the commercial real estate sector, Ladder Capital makes investments in commercial real estate debt securities as well as net-lease equity. By far the most important segment for Ladder Capital, however, is the loan business.

Ladder Capital had $4.0B in loans on its balance sheet as of the end of September 2022, meaning the mortgage REIT’s loan portfolio has shrunk by $600M in the last year. The reason for this reduced balance sheet size is that the REIT has cut back on lending to the commercial real estate sector due to the rise in interest costs associated with new CRE debt as well as concerns over CRE loan performance at a time when interest rates reached record highs.

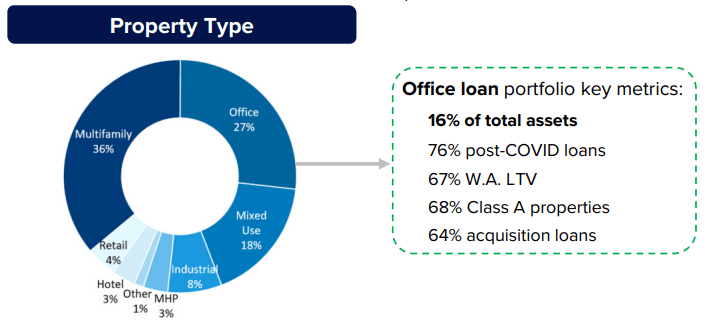

If we look at Ladder Capital’s loan sector breakdown we can see that the mortgage REIT made 27% of its total loan investments in the office sector… which is a relative large percentage. In terms of total assets, 16% of investments related to offices. For comparison, Starwood Property Trust had 13% of its total investments in offices (3% outside of the U.S.).

Ladder Capital’s CRE equity investments includes 156 commercial net-lease properties that are leased to tenants in return for recurring rental income. The segment in total had $888M in assets and generated approximately $55M in net operating income on an annual basis. In this segment, 22% of investments related to offices, so Ladder Capital may be set for some headwinds here if the U.S. office sector underperforms in 2024. As I said earlier, the Federal Reserve’s bid to lower interest rates next year may have the effect of easing pressures on the U.S. office real estate market.

Ladder Capital

Lastly, Ladder Capital’s investments include a $477M securities portfolio, which generates income for the mortgage REIT as well. The securities portfolio consists largely of investment-grade rated commercial real estate securities with a weighted-average duration of 2.1 years.

Ladder Capital

Solid distributable earnings trajectory

Ladder Capital supplies a reasonably safe dividend for the time being, and I don’t see any major risks that could imperil the REIT’s ability to pay its quarterly $0.23 per-share dividend. In the first nine months of FY 2023, Ladder Capital achieved 1.48X dividend coverage (1.35X in Q3’23), so the dividend should be maintained in FY 2024. I don’t see major dividend growth for the REIT, however, as operating conditions in the office market will likely remain weak in the short term as hybrid work conditions and pressure on occupancy rates persist.

Ladder Capital

Priced at book value

In 2021, which is when commercial REITs were still reeling from the COVID-19 pandemic and from a broad-scale shutdown of commercial real estate across the country, I recommended Ladder Capital as a buy. The situation since has improved in such a way that shares of Ladder Capital are now trading close to book value. This is generally true for other mortgage REITs as well, including Starwood Property Trust (STWD)… which I prefer over Ladder Capital given that the REIT has a stronger dividend history and is more diversified in its real estate portfolio: A Solid 10% Yield Waits For Dividend Investors.

Shares of Ladder Capital now also trade above their 3-year average P/B ratio of 0.92X. Back in 2021 I expected that Ladder Capital could erase the gap that existed at the time between share price and book value. With a P/B ratio of 0.96X, I see limited upside ahead. Ladder Capital’s book value for Q3’23 was $12.13 which I consider to be the REIT’s fair value.

Risks with Ladder Capital

The Federal Reserve announced a major pivot in December, which is good news for the commercial real estate market in general. Lenders have been worried about the fallout from higher interest rates and set more capital aside to cushion the blow. As long as interests rates haven’t corrected to the downside, however, Ladder Capital continues to deal with the risk of higher loan defaults.

Final thoughts

Ladder Capital is not a buy right now, in my opinion, but a hold. While the commercial REIT was a speculative buy back in 2021, during the last major crisis in the commercial real estate market, the situation today is quite different. Ladder Capital does offer a well-supported dividend, but since shares now trade at just about reported book value for Q3’23, I believe the risk profile at the current valuation level is not enticing. I also believe, however, that the quarterly dividend is sustainable at its current rate of $0.23 per-share, but I wouldn’t expect a whole lot of the REIT in terms of dividend growth in FY 2024!

{kind=link}

{kind=link}