")

PM Images

The PIMCO High Income Fund (NYSE:PHK) is a closed-end fund that income-focused investors can employ as a means of achieving their goals. This seems only logical given that the name of the fund strongly implies that its intent is to provide its shareholders with a very high level of current income. The fund actually does pretty well here, as it yields 12.03% at the current share price, which is likely to be an incredibly attractive yield for anyone who is still accustomed to 7% or so being a “high yield” as was the case over most of the past fifteen years. However, the fund’s 12.03% current yield is a bit lower than many other closed-end funds that are employing a similar strategy:

|

Fund Name |

Morningstar Classification |

Current Yield |

|

PIMCO High Income Fund |

Fixed Income-Taxable-Multi-Sector |

12.03% |

|

Guggenheim Strategic Opportunities Fund (GOF) |

Fixed Income-Taxable-Multi-Sector |

15.02% |

|

DoubleLine Yield Opportunities Fund (DLY) |

Fixed Income-Taxable-Multi-Sector |

9.18% |

|

TCW Strategic Income Fund (TSI) |

Fixed Income-Taxable-Multi-Sector |

5.22% |

|

Western Asset Diversified Income Fund (WDI) |

Fixed Income-Taxable-Multi-Sector |

12.20% |

|

Virtus Global Multi-Sector Income Fund (VGI) |

Fixed Income-Taxable-Multi-Sector |

13.20% |

As we can see, with the notable exception of the DoubleLine Yield Opportunities Fund and the TCW Strategic Income Fund, most of these funds beat the PIMCO High Income Fund in terms of yield. In some cases, the difference is slight, as relatively small price movements could put the Western Asset Diversified Income Fund below the PIMCO High Income Fund, but in other cases, the difference is much more pronounced. This is something that may prove to be a bit of a turn-off for any investor who is seeking to maximize the income that they earn from the assets in their portfolios. However, there are cases in which an outsized yield is a bad sign, as it suggests that the market believes that a given fund will not be able to sustain its distribution. In this respect, the PIMCO High Income Fund’s relatively average yield may be attractive.

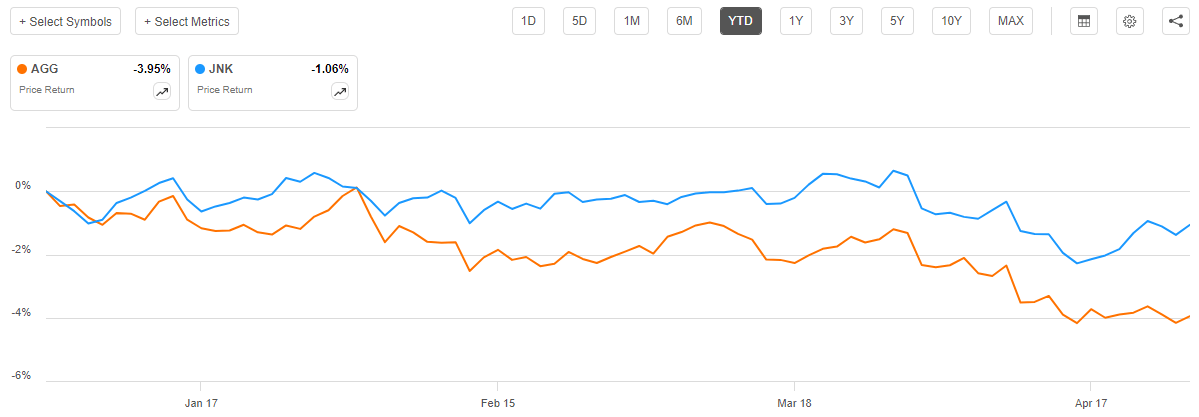

As regular readers can likely remember, we previously discussed the PIMCO High Income Fund in the middle of September 2023. The market since that time has been mixed, as both September and October 2023 were characterized by rising yields and generally falling fixed-income prices. The same has been the case year-to-date, as both the Bloomberg U.S. Aggregate Bond Index (AGG) and the Bloomberg High Yield Very Liquid Index (JNK) are down since the start of the year:

This is mostly a fallout from the final two months of last year, in which various market participants were expecting that the Federal Reserve would significantly cut interest rates in 2024 and so were bidding up fixed-income prices in anticipation of such rate cuts. As economic data since the start of the year has been showing signs of worsening inflation and possibly even stagflation, those expectations have been dashed, and now few bond investors are still expecting much in the way of interest rate cuts.

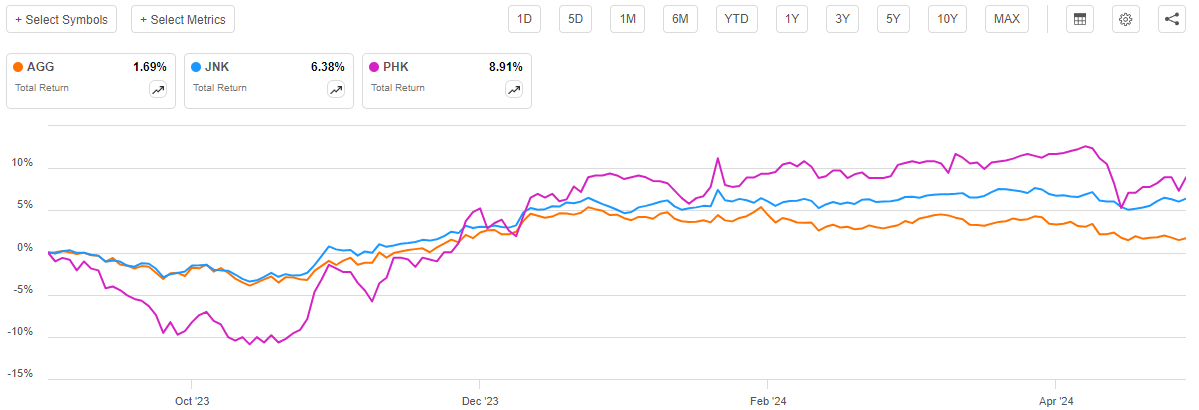

Thus, since we previously discussed the PIMCO High Income Fund, there were two or three months of rising fixed-income prices with the remainder of the intervening period sharply negative for bonds. As such, we might expect that the fund’s share price performance has not been especially attractive since the date of our previous discussion. This is indeed the case, although the PIMCO High Income Fund has outperformed both the domestic investment-grade and junk bond indices. My previous article on this fund was published on September 11, 2023, and since that time the shares of the fund are up 1.48%:

We can clearly see that the fund’s shares managed to beat either of the indices, although it exhibited considerably more volatility. In particular, this fund declined far more than either of the indices during October 2023 and then rebounded much more sharply. When we consider that the fund employs leverage as part of its strategy, this is something that we would expect.

As I have pointed out in various previous articles, such as this one:

A cursory look at a fund’s share price performance does not really provide an accurate picture of what investors in the fund actually received. This is because bonds deliver a significant portion of their investment return in the form of direct payments to their holders. The PIMCO High Income Fund, as with all closed-end funds, pays out all of its investment profits to the shareholders and aims to keep its portfolio value relatively stable over the long term. As such, we need to include the distribution into our analysis to determine the return that investors actually received.

When we include the distributions that the PIMCO High Income Fund paid out into the performance chart above, we see that investors in this fund received an 8.91% total return since mid-September 2023:

Obviously, this total return beat both of the domestic bond indices by quite a lot. That is not unusual, though, as closed-end bond funds usually manage to outperform their index fund brethren due to their significantly higher yields.

However, it is always important to keep in mind that a fund’s past performance is no guarantee of future results. In addition, anyone who purchases shares of the fund today will not benefit from events that occurred in the past. As such, we should have a look at the fund’s assets and positioning today in order to perform an analysis of where it could be tomorrow. This could be particularly important today as several months have passed since we last discussed this fund, so many things have changed. In particular, the fund has released an updated financial report that we will want to take a look at. We will perform that analysis over the remainder of this article.

About The Fund

According to the fund’s website, the PIMCO High Income Fund has the primary objective of providing its investors with a very high level of current income. This makes a lot of sense given the strategy that the fund employs in an attempt to achieve this objective. As is usually the case with PIMCO funds, the website provides a very good description of this strategy:

Using a dynamic asset allocation strategy among multiple fixed income sectors in the credit markets, the fund seeks high current income with capital appreciation as a secondary objective.

Aiming to identify securities that provide high current income and/or capital appreciation, the fund focuses on duration management, credit quality analysis, risk management techniques and broad diversification among issuers, industries and sectors as well as other risk management techniques designed to manage default risk.

The fund may invest any portion of its assets (or none) in below-investment-grade securities, or high yield bonds (also known as junk bonds). The fund will not invest more than 25% of total assets in non-U.S.-dollar-denominated securities. The fund will not invest more than 40% of total assets in securities of issuers located in emerging market countries. Additionally, the fund will normally maintain an average portfolio duration of between zero and eight years.

The final paragraph in this quote is perhaps the most important in describing the fund’s strategy. In short, the fund can invest in pretty much any debt securities that it wants with a few caveats. In particular, the fund has limitations on its ability to invest in bonds with coupon payments in a foreign currency or bonds that are issued by entities in emerging markets. Otherwise, though, it largely has the ability to invest in whatever debt security its management believes will provide its investors with an appropriate balance of high income and appropriate risk.

In my previous article on this fund, I pointed out that the provision of current income is an appropriate objective for any fund that primarily invests in bonds or other debt securities:

The most important thing to consider right now is that the PIMCO High Income Fund is a fixed-income fund, and as the name implies, fixed-income securities deliver the overwhelming majority of their investment return in the form of direct payments to their investors. After all, a bond investor will purchase a bond at face value when it is first issued, receive a regular coupon payment from that bond, and then receive face value again when the bond matures. The coupon payment is the only net investment return that these securities deliver over their lifetimes.

Naturally, there are many different types of bonds and some of them can deliver capital gains in certain circumstances. For example, a bond that is denominated in a currency other than the U.S. dollar can deliver capital gains over its lifetime if the value of the U.S. dollar goes down against the foreign currency. This mostly comes from the fact that an investor had to convert fewer dollars into foreign currency to purchase the bond than they get back following the conversion at maturity. This fund is capable of exploiting this to an extent, which could be an attractive feature today. After all, in a recent article, I pointed out that the long-term fundamentals of the U.S. dollar are not particularly good relative to some foreign currencies. This is mostly due to a combination of the precarious state of Federal government finances and a desire of the BRICS commodity-heavy nations to diversify away from the U.S. dollar. The description of the fund’s strategy states that it will invest no more than 25% of its assets in foreign currency bonds, however, so the PIMCO High Income Fund cannot take advantage of this to the degree that a pure foreign bond fund might be able to. This is still much better than a U.S. dollar-only bond fund would be able to do, though.

The website does not state exactly what percentage of the fund’s assets are currently invested in foreign currency bonds. It only provides this chart, which states that 87.66% of the securities held in the fund’s portfolio are invested in bonds from American issuers:

PIMCO

Obviously, any bond from an American issuer will pay its coupons in U.S. dollars. Investors will also receive the face value maturity payment in the form of U.S. dollars. So, it does not look like the fund currently has much to offer someone who is looking to diversify their currency exposure.

The fund’s semi-annual report likewise does not provide a breakdown of its bond holdings by currency denomination. The report does show that the fund held some foreign currencies as well as currency forwards in its portfolio, so it is definitely investing in some foreign currency bonds, but it does not state to what degree such bonds are included in the entire portfolio. The website explicitly states that it will never have more than 25% of its assets invested in non-U.S.-dollar-denominated bonds and the country holdings chart shows 12.34% of assets in foreign bonds on a market-value basis and 19.75% on a duration-weighted exposure basis. As such, it looks like somewhere between 10% and 20% of this fund’s assets are generally going to be in foreign currency-denominated bonds, with most of that being in developed market currencies. As such, this fund does not look like the best choice for an investor who wants to increase their foreign exposure and take advantage of the declining U.S. dollar thesis. However, it does still do much better than many other fixed-income funds that only invest in domestic securities.

As mentioned in the introduction, investors expected that the Federal Reserve would rapidly cut interest rates in 2024 back at the start of this year. At the time, the market was pricing in six 25-basis points cuts. Today, this seems less likely as inflation has risen every single month so far this year:

This suggests that reducing interest rates could be a very bad idea, as it could cause the already bad inflation situation to become much worse. After all, as we all remember, the original reason why the Federal Reserve started raising interest rates in 2022 was to try and reduce the inflation that was in the economy at that time.

The market has realized that the central bank is unlikely to cut interest rates in the current environment, and so it has pared back its expectations. The FedWatch tool from the Chicago Mercantile Exchange is the usual way that we gauge market sentiment regarding interest rates, as it is based on fed funds futures trading in the market. Here are the probabilities that it puts for the end-of-year federal funds rate today:

The current federal funds target range is 525 to 550 basis points. The market is projecting a 20.2% probability that there will be zero cuts this year and a 39.5% probability of a single 25-basis point cut. Thus, it appears that the market is leaning the most towards only a single interest rate cut over the remainder of 2024. As this is a far more hawkish assumption than what existed at the start of the year, we can quickly see why bonds have declined since January.

This suggests that any damage to the fund’s portfolio that is likely to occur because of changing interest rate expectations has been done. However, there could still be some risks here. After all, there are some Federal Reserve officials saying that rate hikes are on the table. As CNN pointed out earlier this month:

Fed Governor Michelle Bowman, arguably the central bank’s most hawkish voice, recently said that she would favor a rate hike “should progress on inflation stall or even reverse.”

Ms. Bowman is one of the individuals who votes on monetary policy, so her stance is something that bond investors should not ignore. The statement quoted above was made before last week’s economic data release that showed a steep decline in gross domestic product growth along with an acceleration in the growth rate of the personal consumption expenditures index. That suggests stagflation, and after the developments that have been seen with the inflation data this year, certainly seems to meet Ms. Bowman’s qualifications for a rate hike. Thus, it is still quite possible that bonds will suffer another punishment over the next few months, so investors in bond funds such as the PIMCO High Income Fund may not be out of the woods yet.

With that said, the PIMCO High Income Fund can invest all over the bond and debt securities universe, including in floating-rate securities. The semi-annual report puts its holdings as follows:

|

Security Type |

% of Portfolio |

|

Loan Participations and Assignments |

22.9% |

|

Corporate Bonds & Notes |

37.9% |

|

Convertible Bonds & Notes |

0.4% |

|

Municipal Bonds & Notes |

5.3% |

|

U.S. Government Agencies |

2.0% |

|

Non-Agency Mortgage-Backed Securities |

14.1% |

|

Asset-Backed Securities |

7.9% |

|

Sovereign Issues |

3.2% |

|

Common Stock |

11.5% |

|

Warrants |

0.0% |

|

Preferred Stock |

3.7% |

|

Real Estate Investment Trusts |

0.6% |

|

Short-Term Instruments |

0.8% |

|

American Money Market |

10.9% |

Some of the loan participations as well as the money market instruments are floating-rate securities. As I have pointed out in the past, these securities do not experience much in the way of price changes when interest rates go up. Thus, the fact that the fund is holding some things such as this should provide it with better protection against a potential interest rate hike than a fund that is invested in straight bonds. However, we can still see that the majority of the fund’s holdings are in traditional fixed-rate bonds, so it seems likely that it could suffer a decline should inflation continue to come in hot and cast further doubt on the likelihood of even a single interest rate cut.

Leverage

As is the case with most closed-end funds, and as was mentioned in the introduction to this article, the PIMCO High Income Fund employs leverage as a method of boosting the effective yield that it earns from the assets in its portfolio. I explained how this works in my previous article on this fund:

In short, this fund is borrowing money and then using these borrowed funds to purchase bonds and other income-producing assets. As long as the interest rate that the fund pays on the borrowed money is less than the yield that it receives from the purchased assets, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As a result of this, we want to be sure that the fund is not employing too much leverage because that would expose us to an excessive amount of risk. I generally do not like to see a fund’s leverage exceed a third as a percentage of its assets for this reason.

As of the time of writing, the PIMCO High Income Fund has leveraged assets comprising 20.32% of its portfolio. This represents an increase over the 17.69% leverage that the fund had the last time that we discussed it, which is surprising since the share price has increased since that date. The fund’s net asset value is also up since that time, rising 4.33% since the date that the previous article was published:

Barchart

Ordinarily, when a fund’s net asset value rises, its leverage goes down. This is because an increase in net asset value means that the size of the fund’s portfolio increased. Thus, the outstanding borrowings as a percentage of the portfolio would normally decrease, all else being equal. The fact that this fund’s leverage went up along with its net asset value suggests that the fund actually borrowed more money. This is not necessarily a bad thing as it should still increase the effective yield that shareholders receive, but it is somewhat surprising because few other funds have actually been increasing their leverage.

Here is how the leverage of the PIMCO High Income Fund compares to that of its peers:

|

Fund Name |

Leverage Ratio |

|

PIMCO High Income Fund |

20.32% |

|

Guggenheim Strategic Opportunities Fund |

19.70% |

|

DoubleLine Yield Opportunities Fund |

19.34% |

|

TCW Strategic Income Fund |

0.00% |

|

Western Asset Diversified Income Fund |

31.30% |

|

Virtus Global Multi-Sector Income Fund |

30.47% |

(all figures from CEF Data)

As we can clearly see, the PIMCO High Income Fund has a leverage ratio that generally compares pretty well with its peers. It is substantially lower than both the Western Asset Diversified Income Fund and the Virtus Global Multi-Sector Income Fund. While the PIMCO High Income Fund does have more leverage than both of the Guggenheim Strategic Opportunities Fund and the DoubleLine Yield Opportunities Fund, it is not very much higher in this respect. The TCW Strategic Income Fund is not comparable because that fund does not use leverage.

Overall, the takeaway here seems to be that we should not need to worry too much about the leverage that is employed by the PIMCO High Income Fund. While it is certainly true that this fund has increased its leverage over the past few months, it remains very much in line with its peers. As such, the balance between the risks and the potential rewards that come with leverage appears to be reasonable here.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the PIMCO High Income Fund is to provide its investors with a very high level of income. In pursuit of this objective, the fund has invested its assets into a portfolio that consists primarily of both investment-grade and high-yield bonds from domestic and foreign issuers. Bonds and other debt securities primarily deliver their investment returns in the form of direct payments to their owners, which in this case is the fund. The PIMCO High Income Fund collects the payments that it receives from these securities, and then borrows money in order to purchase and collect payments from more securities than it can afford solely with its own equity capital. This has the effect of boosting the effective yield of the fund’s portfolio by the difference between the coupon rate of the purchased bonds and the interest rate that it needs to pay on the borrowed money. The fund combines the money that it receives from this source with any profits that it manages to achieve by exploiting the fact that bond prices move when interest rates change, as well as the occasional profit from foreign currency movements. The fund ultimately pays out all of the money that it earns from all of these various sources to its investors, net of its expenses. When we consider that bond yields today are higher than they have been on average in many years and combine that with the impact of leverage and trading profits, we can make the assumption that the fund’s shares should be able to boast a reasonably high yield today.

This is indeed the case, as the PIMCO High Income Fund pays a monthly distribution of $0.0480 per share ($0.576 per share annually). This gives the fund a 12.03% yield at the current price. As was shown in the introduction, this yield is certainly decent, although it is far from the most attractive yield that can be obtained among its peer group. The fund has unfortunately not been particularly consistent with respect to its distributions over the years. As we can see here, the PIMCO High Income Fund has cut its payout several times since its inception, reducing its payout over time:

CEF Connect

This is something that will undoubtedly be a turn-off to those investors who are seeking a safe and consistent income that can be used to pay their bills or finance their portfolios. However, we do see that this fund has not cut its distribution since 2020, which gives it a slightly better track record in the post-pandemic period than many other bond funds. A lot of fixed-income funds took fairly large losses in 2022 as a result of monetary policy changes. For most of the decade or so prior to 2022, interest rates in the United States and other developed nations were incredibly low. When that changed due to rapid increases in short-term rates to fight inflation, bond prices ended up declining significantly and causing losses for many funds that invest in the sector. These funds then cut their distributions to preserve their asset bases. However, this fund did not react similarly, which is somewhat interesting as it is hard to believe that this fund was able to avoid such losses.

As I have pointed out numerous times in the past, a fund’s history of declining distributions is not necessarily something that new investors should focus on. This is because anyone who purchases shares of the fund today will receive the current distribution at the current yield. This individual will not be adversely impacted by events that occurred in the past, and the most important thing is how well the fund can maintain its distribution going forward. Let us investigate that.

Fortunately, we have a fairly recent document that we can consult for the purposes of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the full-year period that ended on December 31, 2023. A link to this document was provided earlier in this article. This is a newer report than the one that was available to us the last time that we discussed this fund, which is very nice to see. This is because this report will provide us with information about the fund’s performance during the two widely divergent markets that existed in the second half of 2023. The first of these occurred during the summer months, which saw falling bond prices and rising bond yields due to the market’s realization that the so-called “monetary policy pivot” that was priced into assets in the first half of the year was very unlikely to actually occur. This lasted until late October, when investors started to think that interest rates would decline rapidly in 2024 and started bidding up prices. While that also appears to be unlikely, the bond market remained very strong through the end of the reporting period. The first of these market environments probably caused this fund to incur some realized or unrealized losses. However, it had the potential for substantial gains during the final two months of the period reflected in the semi-annual report. The financial statements will give us a good idea of how well it handled these environments to the benefit of its investors.

For the six-month period that ended on December 31, 2023, the PIMCO High Income Fund received $1.277 million in dividends and $39.234 million in interest from the assets in its portfolio. When we combine this with a small amount of income from other sources, we arrive at a total investment income of $40.922 million for the six-month period. The fund paid its expenses out of this amount, which left it with $31.484 million available for shareholders. This was, unfortunately, not sufficient to cover the $42.969 million that the fund paid out in distributions over the period. At first glance, this is likely to be very concerning, as we would ordinarily prefer that a fixed-income fund fully cover its distributions with net investment income. This one obviously failed to accomplish that task.

However, there are other methods that a fund can employ to obtain the money that it requires to cover its distributions. In the case of this fund, it could take advantage of the fact that bond prices move inversely to interest rates in order to achieve some capital gains by trading bonds prior to maturity. These are realized capital gains and so are not considered to be investment income for either tax or accounting purposes. However, realized capital gains clearly do represent money coming into a fund that can be paid out to the shareholders.

The PIMCO High Income Fund did enjoy a certain amount of success at obtaining money via this alternative source in the six-month period. It reported net realized losses of $30.773 million, but these were more than offset by $63.255 million net unrealized gains. Overall, the fund’s assets increased by $37.686 million over the six-month period after accounting for all inflows and outflows. Thus, it appears that the fund did manage to full cover its distributions over the period.

However, there are two important caveats here. The first is that the fund only managed to cover its distributions due to net unrealized gains. As we are all well aware, unrealized gains can be quickly erased by any market correction. As such, there is no guarantee that the fund will be able to hold onto the money that it is using to ensure its long-term sustainability. Its net asset value per share is down 1.08% year-to-date, which suggests that it has indeed failed to keep some of its unrealized gains:

Barchart

This also tells us that the fund has failed to cover all of the distributions that it has paid out so far in 2024, which could be a concern. We should keep an eye on this as continued weakness in the bond market, which is a very real possibility, could challenge the fund’s ability to afford its distribution.

Another thing to keep in mind is that the increase in the fund’s assets that we saw in the second half of 2023 was partly due to the issuance of new shares that raised $13.586 million of new money. The fund also got back $4.241 million from existing investors putting their distributions back into the fund. While the fund still would have covered its distribution without this influx of money, its coverage was not as high as it may at first appear.

Valuation

As of April 25, 2024 (the most recent date for which data is available as of the time of writing), the PIMCO High Income Fund has a net asset value of $4.58 per share. However, the shares are currently trading at $4.79 each. This gives the shares a 4.59% premium on net asset value at the current price. This is a bit better than the 5.78% premium that the shares have had on average over the past month.

While the current price is a bit more reasonable than normal, it is still important to keep in mind that anyone buying the fund at the current price is essentially purchasing the bonds that it holds for much more than they are actually worth. As such, this is definitely not a value-priced fund and there could be some risks associated with overpaying for its assets. In particular, a decline that swings the price to a discount could result in some large losses. As such, any potential investor should think carefully before buying the fund at this price.

Conclusion

In conclusion, the PIMCO High Income Fund is a reasonably decent bond fund for investors in search of income. The fact that this fund might include non-U.S. dollar bonds alone is a nice feature, given the poor long-term fundamentals of the U.S. dollar today. The fund also seems reasonably well-diversified and does not employ a substantial amount of leverage. The only real concerns here are that it has failed to cover its distribution year-to-date and that it is trading at a discount. It seems highly unlikely that bonds will rebound given the current economic data, so it is possible that investors purchasing today may experience some share price declines.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}